If you’ve been following the financial headlines lately, you’ve probably heard the word “stagflation” more than once. It’s a term that means something very specific—and something most investors haven’t had to seriously contend with for four decades. In our Q2 2026 Quarterly Market Report webinar, BIP Wealth’s Chief Investment Officer, Eric Cramer, CFP®, CFA®, walked through what happened in markets during the first quarter, where he thinks inflation and economic growth are headed, and why now is exactly the right time to stay disciplined.

Here’s a summary of Eric’s main talking points for this quarter. You can also watch the full recording of the webinar below.

The Top U.S. Stocks Got Hobbled—Again

What happened in 2025 is turning out to be the template for what’s happening in 2026. High valuations with these top 10 stocks, big sell-off in the first quarter, and then a rally to begin to bring most of these back.

Source: Morningstar, Worldperatio.com. PE Data as of 12/31/2025, Returns as of 3/31/2026. For illustrative purposes only. Past performance is not a guarantee of future results.

If you followed our Annual Market Report earlier this year, this story will feel familiar. The top 10 U.S. stocks—companies like Apple, Microsoft, NVIDIA, and Meta—now represent roughly 40% of the total U.S. market. They entered 2026 with elevated valuations, and in Q1 they paid for it: nearly every name on that list posted significant negative returns, some by double digits.

The good news? Just like in 2025, these stocks have largely started to recover as Q2 has unfolded. The pattern is holding: high valuations, a Q1 selloff, then a rebound. That doesn’t mean Eric is comfortable with those valuations, it just means staying diversified and staying invested has, once again, been the right call.

For the broader market, the MSCI ACWI IMI Global Equity Net Index was down 2.75% in Q1. Fixed income was essentially flat. If you’re diversified across asset classes and geographies, you likely weathered the quarter without much drama.

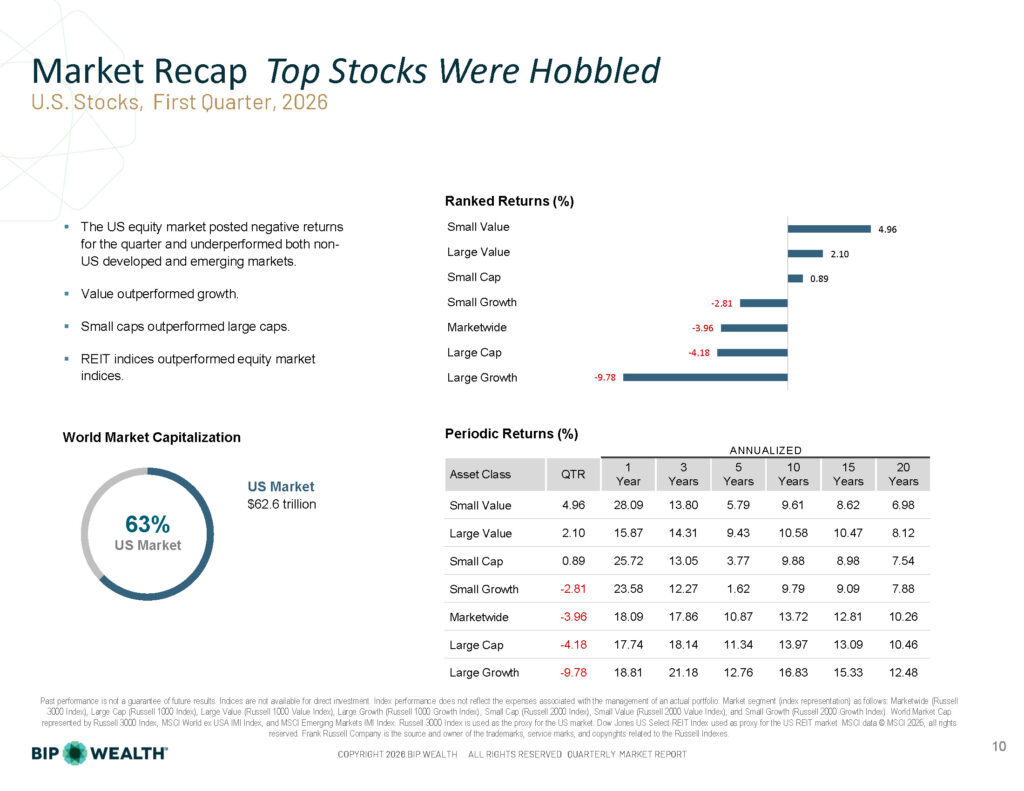

Value Led. Emerging Markets Led. The U.S. Trailed.

Source: Russell/MSCI. For illustrative purposes only. Past performance is not a guarantee of future results. Indices are not available for direct investment.

This quarter confirmed a trend we’ve been tracking for several quarters now: the U.S. has not been the best place to invest. That’s not a permanent indictment—we still maintain a modest U.S. overweight, as most advisors do—but the data keeps pointing in the same direction.

Within the U.S., value outperformed growth and small caps outperformed large caps. These are results broadly consistent with what long-term historical data would predict. Small Value returned +4.96% for the quarter while Large Growth fell -9.78%. This is exactly what we’d expect when the high-flying, high-valuation names run out of momentum.

Overseas, the story was similar. International developed markets declined modestly in USD terms but still outperformed the U.S. Emerging markets, despite posting slightly negative Q1 returns, and have had a standout trailing year. As mentioned in a previous blog from Eric, Emerging markets have quietly continued to lead the recovery in Q2 so far.

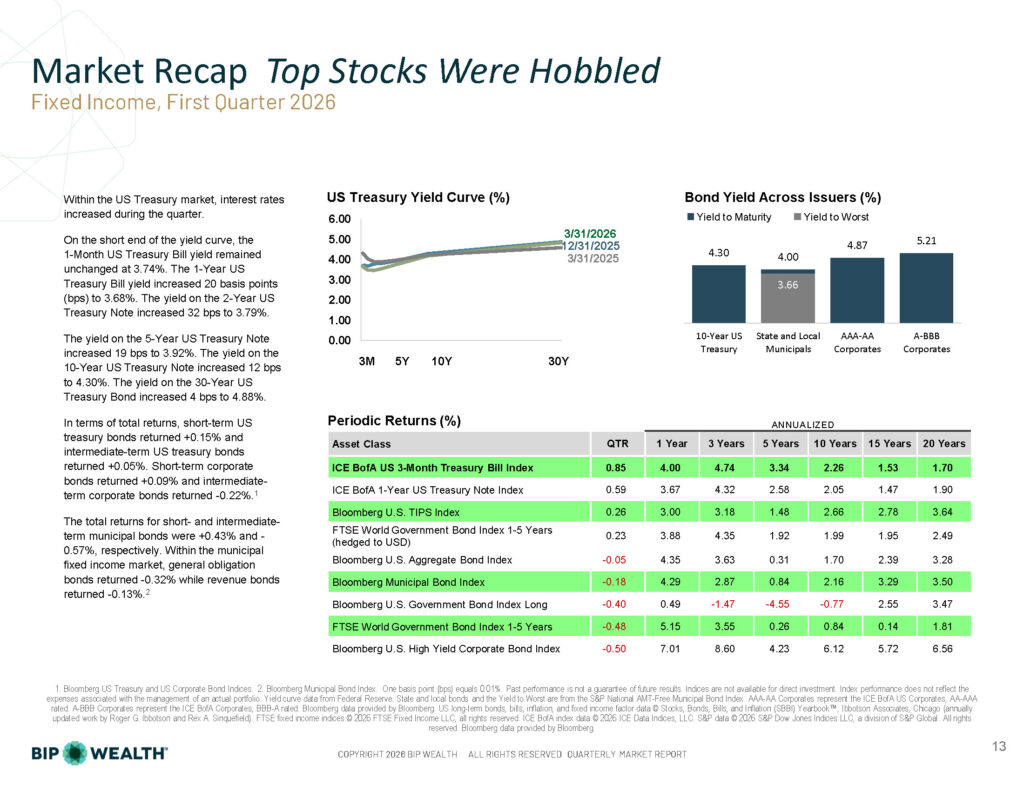

The Yield Curve Is Looking Relatively Normal

Source: Federal Reserve. For illustrative purposes only.

One thing Eric pointed out that doesn’t always get attention: the yield curve is looking reasonably normal right now. Short-term rates are lower than long-term rates, which is exactly how it’s supposed to work. When we see severe distortions on the short end of the curve, it usually signals the Fed is either too aggressive or too loose. Right now, the market seems to believe the Fed’s posture is appropriate.

That said, rates did tick up across most maturities during the quarter: the 10-Year Treasury yield moved to 4.30%, and the 30-Year to 4.88%. For clients near or in retirement who rely on fixed income, the one-year return on the Bloomberg U.S. Aggregate of 4.35% is reasonable. But to be clear, over a 10- or 20-year horizon, the real risk is being too conservative. Equities have historically delivered meaningful premiums over fixed income over long periods, and that relationship held again over every multi-year period shown in our blended benchmark data.

So, Is Stagflation Coming?

This is the big question. Eric doesn’t know the answer yet, and he’s not convinced anyone else does either. But it’s important to understand what we’re watching and why it matters.

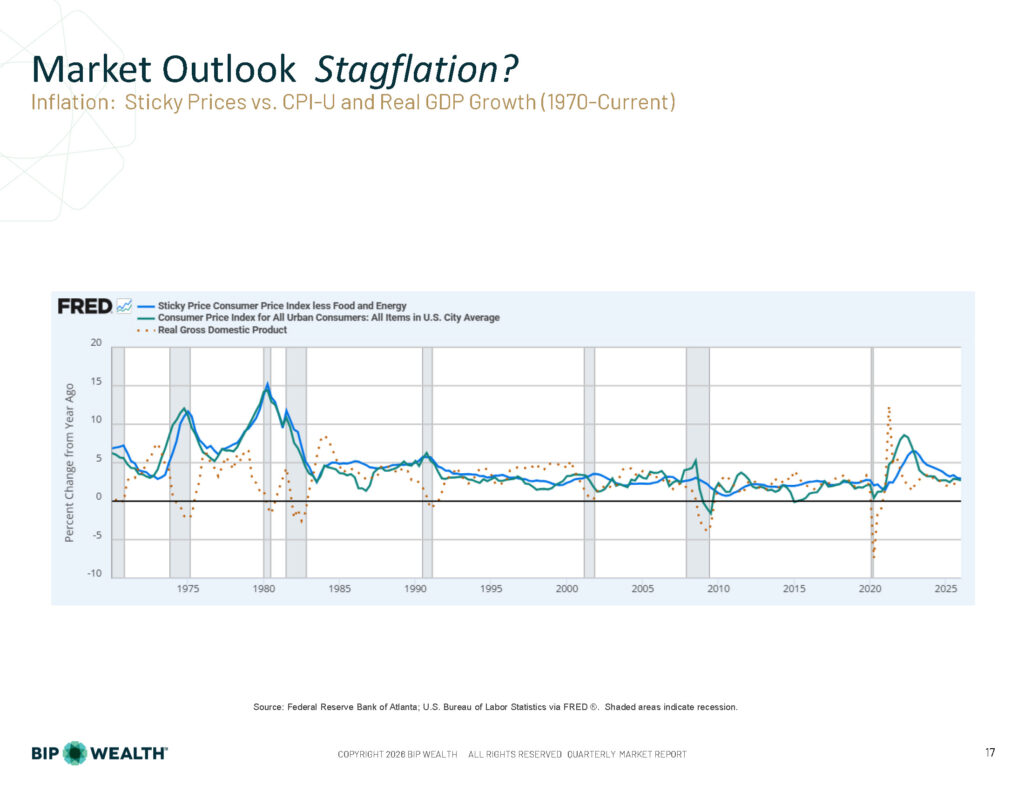

Stagflation occurs when economic growth slows at the same time inflation rises. It’s a particularly painful combination because the normal policy tools work against each other—cutting rates to spur growth can make inflation worse; raising rates to fight inflation can suppress growth further. We saw it in the 1970s and early 1980s, and it was rough.

Here’s what concerns Eric right now:

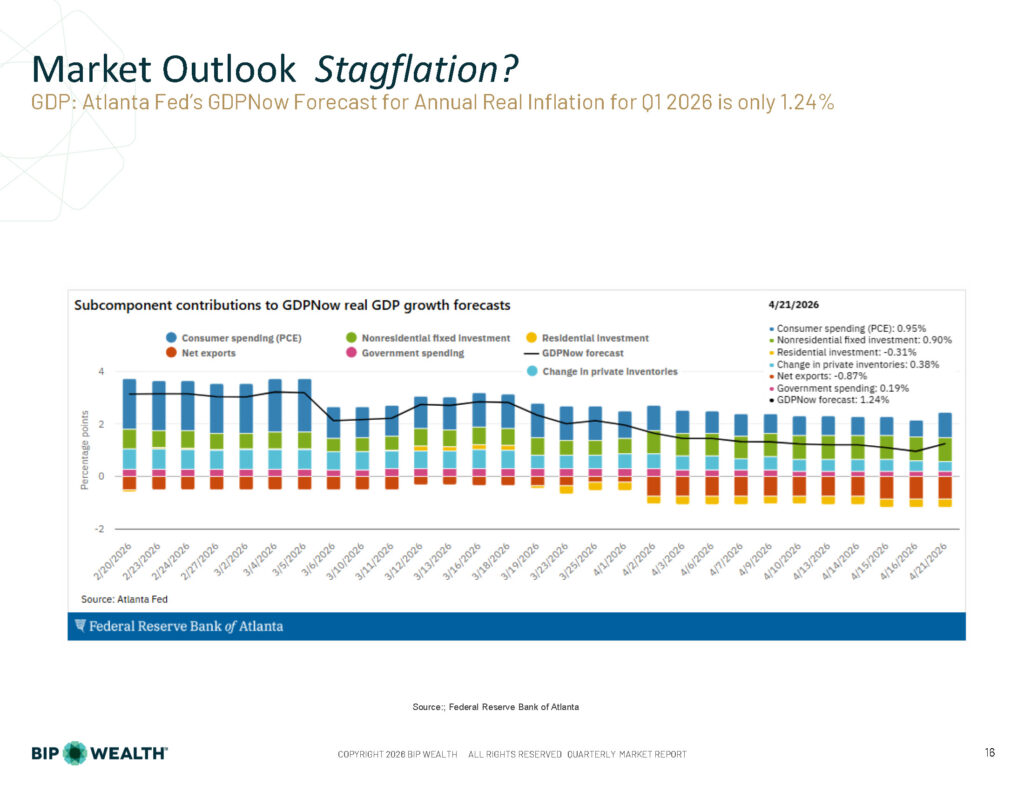

Economic growth may be softening. The Atlanta Fed’s GDPNow model was forecasting just 1.24% real GDP growth for Q1 as of late April (though that number has since climbed back toward 3.5%, a reminder of how volatile real-time forecasts are). Reliable GDP data is always a year behind by the time it’s been revised; we’re navigating with incomplete maps.

Source: Federal Reserve Bank of Atlanta. For illustrative purposes only.

Inflation may be picking up. CPI data has become less reliable than it used to be: survey response rates are down, and some government data collection has been underfunded. But the trajectory appears to be moving higher. If we look at the historical record going back to 1970, virtually every major inflation spike has been followed by a recession. The one exception in recent memory was post-COVID, and we were right at the time to say we didn’t think a recession was coming. We were right then. Whether that holds again is less certain.

“If you start to see inflation spike in the near term, most of the time that means we’re going to have a recession. So we’re certainly watching out for it.”

Source: Federal Reserve Bank of Atlanta; U.S. Bureau of Labor Statistics via FRED®. Shaded areas indicate recessions.

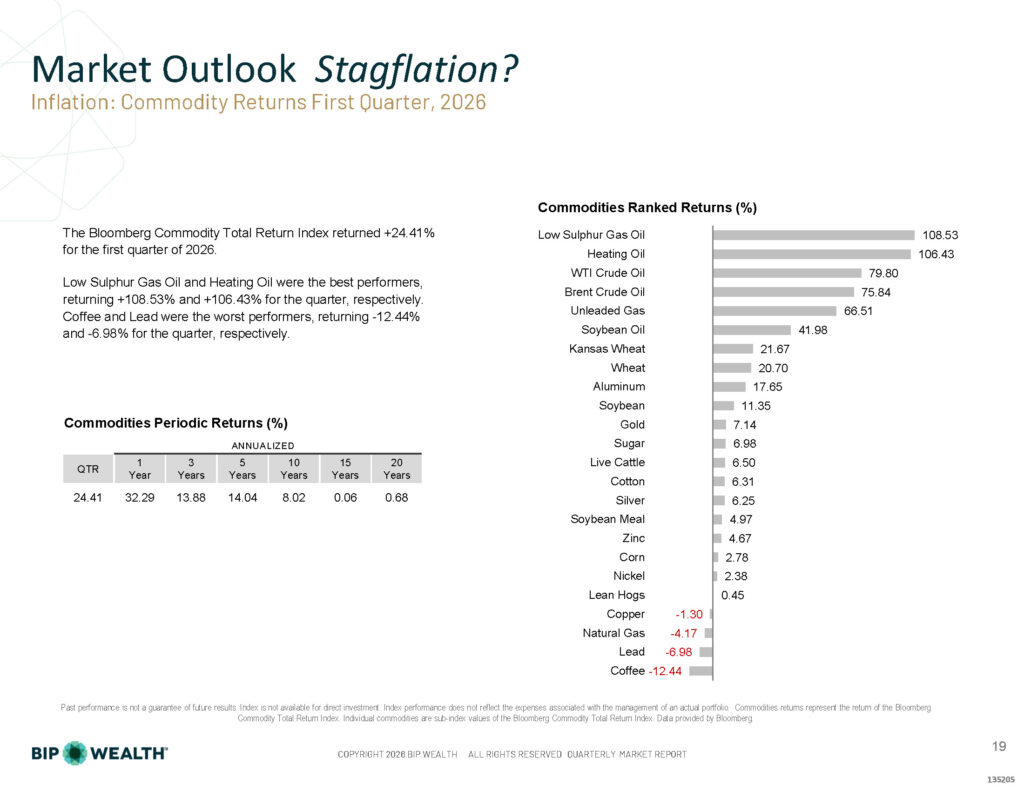

Commodity Prices Are Sending a Warning

Source: Bloomberg Commodity Total Return Index. For illustrative purposes only. Past performance is not a guarantee of future results.

The Bloomberg Commodity Total Return Index returned +24.41% in Q1 2026. That number alone should get your attention. Energy led the way with Low Sulphur Gas Oil and Heating Oil each roughly doubled in the quarter. Crude oil was not far behind.

One nuance worth calling out: the spot price of oil and the futures price are not the same thing, and much of what gets reported in financial media reflects futures prices. At the beginning of April, the Europe Brent spot price hit around $127 per barrel—roughly $30 higher than futures at the time. Some refineries around the world were paying $150–175 per barrel in isolated transactions on the spot market. That difference matters; it’s what actually hits consumers and businesses in the short term.

Add to that the fact that the Strait of Hormuz disruptions continue to affect supply chains, and you have a recipe for continued inflationary pressure in the quarters ahead.

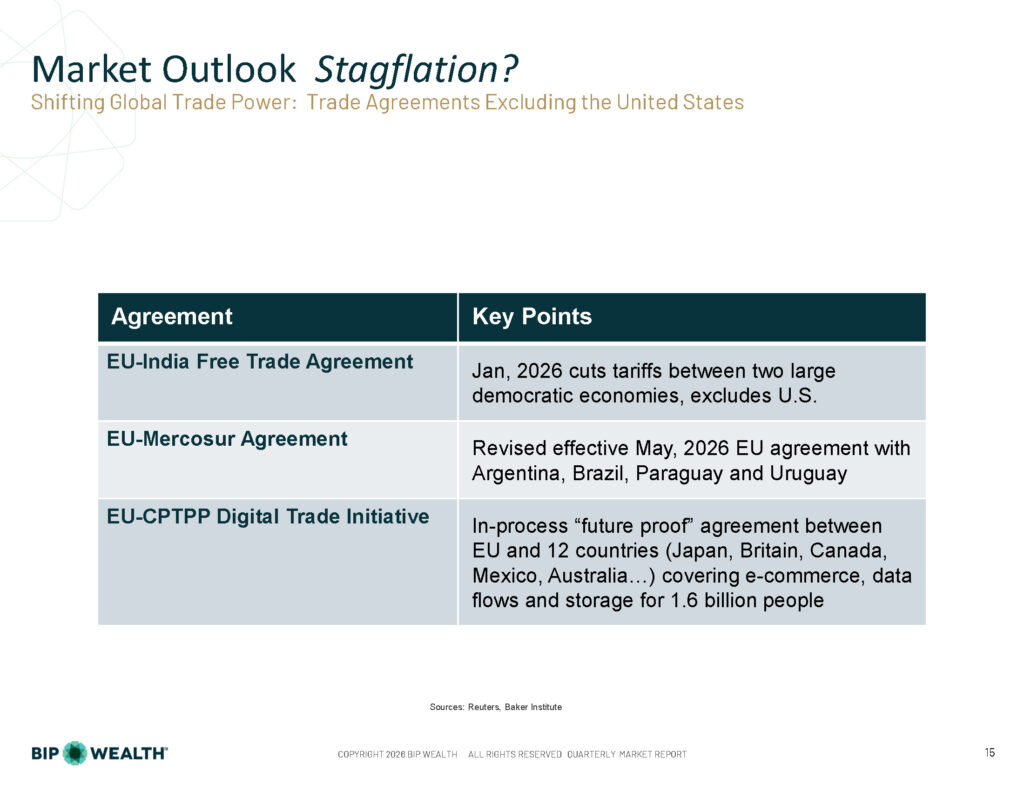

Global Trade Power Is Shifting and the U.S. May Be on the Outside

One of our four key themes for 2026 is “Shifting Global Trade Power,” and Q1 gave us more evidence that this trend is accelerating.

Sources: Reuters, Baker Institute.

Three significant trade agreements—the EU-India Free Trade Agreement, the revised EU-Mercosur Agreement, and the in-progress EU-CPTPP Digital Trade Initiative—are all designed to chart a course that doesn’t depend on U.S. participation. I remember watching something similar happen after COVID, when global companies scrambled to reduce their reliance on Chinese supply chains. What we’re seeing now is a version of that, but applied to U.S. economic policy uncertainty.

All parties are making moves to protect what they perceive is in their own best interests. And the net effect of that could be that the United States is just becoming more and more isolated.

“This isn’t necessarily a catastrophe. But it does mean the environment is changing, and investors should expect the data to look different going forward: more volatility in the dollar, more pressure on trade-sensitive sectors, and potentially lower long-run U.S. growth relative to international markets.”

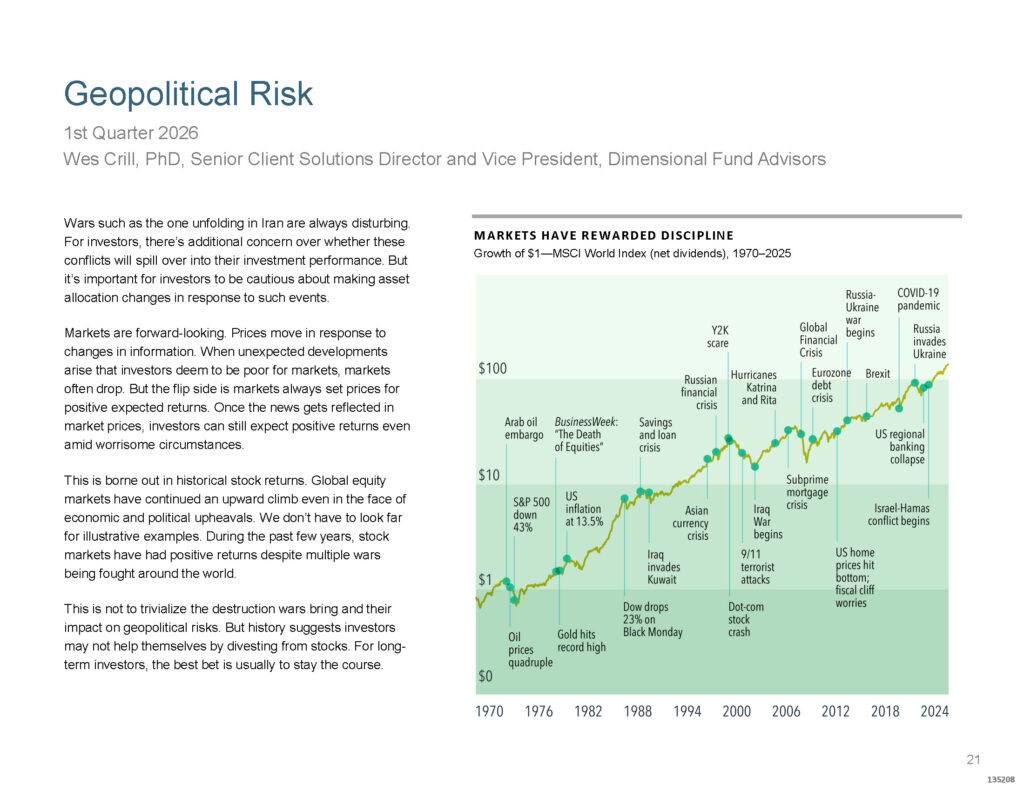

History Has Rewarded the Patient Investor

Source: Dimensional Fund Advisors. Past performance is not a guarantee of future results. Index is not available for direct investment.

Eric closed with something worth repeating: current events always feel unsettling when you’re living through them. The Arab oil embargo. Black Monday. 9/11. The Global Financial Crisis. COVID. In every one of those moments, there were credible arguments for why this time was different, why capitalism was broken, why markets would never recover.

They were wrong. Every time.

“Sometimes it’s like standing on the edge of a cliff, waiting for a gust of wind that might blow you over. That’s kind of a normal thing. But democracy, capitalism, property rights, rule of law, and just the innovative spirit of millions of human beings will cause us to be rewarded for our faith in the stock market in the long run.”

We may or may not see stagflation materialize in the quarters ahead. But the conditions worth watching are real, and the right response isn’t to react to every headline. It’s to stay diversified, keep your financial plan current, and make sure your allocation reflects your actual time horizon. If you have questions about how any of this applies to your situation, reach out to us to connect with a BIP Personal Wealth advisor.

This publication contains general investing information that is not suitable for everyone and is subject to change without notice. Past performance is no guarantee of future results and there is no guarantee that any views and opinions expressed will come to pass. Any reference to market or index performance is for informational and illustrative purposes only and does not reflect the deduction of fees and does not represent actual portfolios. The information contained herein should not be construed as personalized investment advice, tax advice, or financial planning advice, and should not be considered a solicitation to buy or sell any security. Investing in the stock market and the bond market involves gains and losses and may not be suitable for all investors.

BIP Wealth, LLC is a registered investment adviser. Registration does not imply a certain level of skill or training. Additional information about BIP Wealth is available on the SEC’s website at www.adviserinfo.sec.gov.