Signed into law on July 4, 2025, the One Big Beautiful Bill Act, OB3 for short, offers comprehensive tax reform that will take effect on January 1, 2026. To help BIP Wealth clients better understand the new laws, our in-house Estate Planning Attorney, Sarah Watchko, and Tax Advisor, CPA, Allie Powell, teamed up to present a recent webinar. In this recap, we’ll review the key points of their presentation, breaking down what changed and what remained unchanged in our tax laws.

The webinar started with an iconic quote from Benjamin Franklin: “Our new Constitution is now established and has an appearance that promises permanency; but in this world nothing can be said to be certain except death and taxes.” Simply put, while these new tax laws come with changes for now, reforms in the future are to be expected, as tax laws are inherently political. So, what do you need to know about the One Big Beautiful Bill Act? In this blog, we’ll break it down for you.

While we could analyze the entire bill word-for-word, we decided to break our webinar into two main categories: Gift & Estate Taxes and Personal Income Taxes. In each section, we discussed what changed vs. what remained the same, compared to the significant reforms passed in the 2017 Tax Cuts & Jobs Reforms Act.

To start, let’s break down what remained the same. Overall, most of the laws surrounding gift & estate taxes remained the same on the federal level. While specific states may have their own estate taxes, portability, annual exclusions, and the basic framework of the 2017 reforms have all been left untouched.

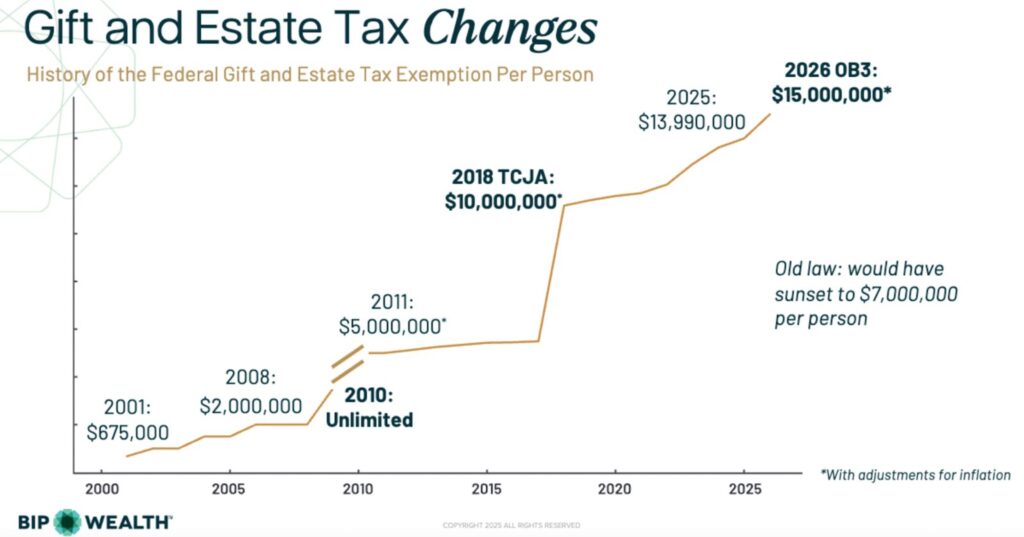

The one big change comes with transfer tax exemptions. Now permanently set at $15 million ($30 million for a married couple), this allows you to transfer assets to a loved one without any taxes being imposed on your estate. For example, if you have $1 billion in assets and gift it all to your spouse during your life, this will not go towards the exemption amount. Plus, with portability remaining unchanged, if the $1 billion is left to your spouse, they can take the $15 million in exemptions with them, thus giving you the $30 million.

Another key tax law that remains unchanged is the annual exclusion. Another way to think about this concept is that the IRS doesn’t want to keep tabs on all of your birthday presents. As of the 2025 fiscal year, any gifts up to $19,000 can go tax-free. And there are no limits on the amount of gifts you can give up to the $15 million exemption.

The chart below tracks how the total exemption amount has increased over time, from just $675,000 per person in 2001.

The impacts of these changes are clear. If your estate is worth under $7 million, or $14 million as a married couple, your estate planning strategies should remain largely unchanged. If your estate is worth between $7 million and $15 million ($14 million and $30 million as a married couple), you are now safer from estate taxes than ever before. If your estate is worth more than $30 million, your strategy would remain largely unchanged. As always, it’s important to regularly consult your tax advisor to ensure your plan continues to adapt to changing financial regulations.

Where the new laws bring a plethora of changes is with personal income tax. Now, this bill was pushed through by Congress. Now, it is up to the IRS to implement each change. OB3 continues a lot of the shifts made in 2017, which at the time was the most significant tax reform since 1986. To set the record straight, Social Security benefits will remain taxable. There were rumors in the media that this was going away, but up to 85% of your future benefits will still be included in your taxable income. That remains unchanged.

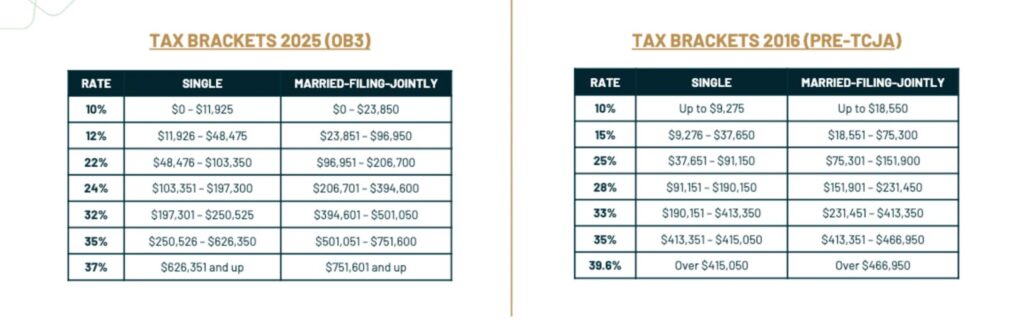

The income tax brackets from 2017 also remain the same, giving working families a bit more security in knowing they’ll likely not be paying more in 2026 and the years to come.

Additionally, the standard deduction for taxes remains much higher, with up to $15,000 for individuals and $30,000 for married-joint filings. This can be used for medical expenses, property taxes, charitable contributions, and more.

Now, what will be changing? The short answer is quite a bit. The State and Local Tax Cap (SALT) for individuals has increased from $10,000 to $40,000. While this law phases out higher earners of $500,000 or more, it will allow you to potentially enjoy higher itemized deductions until 2030. On top of this, Trump Accounts will now be opened for kids born from 2025-2028. The federal government will make an initial $1,000 deposit, with up to $5,000 in annual after-tax contributions until the child reaches 18 years of age. Growth is tax-deferred, with early withdrawals after age 18 subject to a 10% penalty. However, many questions remain about how these accounts will work, what will be sunset in the future, and the overall mechanics, so be sure to discuss this with your tax advisor.

Additional changes include a $6,000 deduction for taxpayers 65 years and older, expansions to eligible expenses for 529 funds, and no taxes on overtime and tips up to $25,000. For business owners, the bill also allows for an alignment of tax-deductible expenses with cash flow, plus the potential for significant capital gains savings through company stock.

If you have any questions about the new OB3 laws or need to take a closer look at your current estate plan, contact the BIP Wealth team today!

Disclaimer: This is a very high-level overview of some of the important aspects of the new tax law. It’s intended for general informational purposes, and it’s not intended to constitute tax, legal or investment advice, so if you need or want tax, legal or investment advice, please consult your personal tax professional or estate planning attorney before making any decisions.

January is the perfect time to start fresh and plan ahead for 2025. From ongoing changes in the market to the recent U.S. Presidential Election, there is a lot for both individuals and business owners to consider when reviewing their financial plans. From refining your investment strategies to ensuring your estate plan is up to date, a comprehensive new year financial checklist and review can uncover opportunities to strengthen your financial foundation. In this blog, we’ll discuss steps you can take to protect your wealth in the new year.

Because your goals act as the foundation for your wealth plan, the new year financial planning checklist is the perfect time to determine if anything needs changing.

Ask yourself a few of these questions: Are you on track to achieve your short- and long-term objectives? Do you need to adjust savings targets, diversify your investments, or reprioritize your spending? Reassessing your goals annually ensures you remain focused, intentional, and adaptable as you navigate the markets.

Although estate planning may seem like it’s only beneficial for those with significant net worths, we’d argue that it is important for everyone to regularly review (or establish). Life changes—such as marriages, divorces, births, or deaths—can impact your wishes, while shifting tax laws may create new opportunities or challenges. While going through your new year financial planning checklist, it may be in your best interest to revisit your estate plan to ensure it reflects your current circumstances and goals.

At BIP Wealth, we consider a wide range of factors when helping our clients plan their estate—from their unique financial goals to Power of Attorney and Healthcare Directives. Together, we’ll assist with your annual review to make sure you minimize your tax bill and help create generational wealth for your family.

While investing is a long-term way to build wealth, it is important to review your portfolio with your wealth manager when going through your new year financial planning checklist. Maintaining the right mix of investments such as small vs. large-cap investments, exchange traded funds (ETFs) vs mutual funds, and private vs. public investments, can help ensure you have a diversified portfolio to weather market fluctuations. During your new year financial planning, you can ensure your investments properly match your financial goals and are risk-tolerant. Rebalancing your portfolio can help restore the intended balance between stocks, bonds, and other asset classes, allowing you to manage risk effectively.

One of the best ways to build long-term wealth is through tax-advantaged accounts, such as 401(k) plans. These accounts enable your money to grow over time without the burden of hefty annual tax bills. In fact, regulatory changes in 2024 allowed investors to commit more money than ever to their plans, ensuring more wealth grows tax-advantaged.

For families, don’t overlook the power of Health Savings Accounts (HSAs), too. These accounts provide a triple tax benefit: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified expenses are tax-free.

If you have children who are planning on going to college, 529 plans are another great option to consider when going through your new year financial planning checklist. By utilizing accounts like these, you can fortify your wealth for the long term.

If you’re a business owner who offers or is looking to offer 401(k) benefits to your employees, it is not a set-and-forget type of strategy. One of the most important small business new year checklist steps is to benchmark your 401(k) plan. Why is this important? This can help you evaluate the costs of your plan and potentially find ways to reduce your tax bill. During the benchmarking process, your financial advisor will help you identify new investment opportunities to meet both your goals and the goals of your employees.

Finally, consider whether you’d like to set money aside for charitable contributions when going through your year-end financial checklist, as they can offer more tax benefits in the new year. You can also take advantage of the annual gift tax exclusion, which allows you to gift up to $18,000 (for 2024) per recipient without incurring gift taxes. If you’re married, you can double this amount by gifting jointly. This is an excellent way to transfer wealth to the next generation while minimizing taxes.

If you’re looking for holistic wealth management services like you read about above, be sure to reach out to our team. You can also check out our resources hub to learn more about the latest topics in the financial world.

It is important to establish a new year financial planning checklist that helps you identify financial planning opportunities, new investment ideas, and ways to minimize taxes. This can help you grow your wealth over time while losing as little to tax bills as possible.

A new year financial planning checklist can help you ensure your goals are being met and that your financial plan is sound.

Yes! For individuals, families, and business owners, consulting a financial advisor here at BIP Wealth can be a great way to simplify the process. Think of our team as your Personal CFO.

In life, things often change in a heartbeat. Unexpected life events can have serious financial consequences if not planned for. Whether it’s a medical emergency, job loss, or natural disaster, being financially prepared for life’s unexpected events is essential. The right planning can make dealing with unexpected life events less stressful, ensure you have proper cash flow, and even protect your wealth in the long term. In this guide, we’ll break down the importance of understanding unexpected life events and how to best plan for them.

Before we dive into strategies for dealing with unexpected life events, let’s first establish what situations you should financially plan for and why they’re important.

Although it is not easy, have you ever imagined a scenario in which a loved one suddenly passes away? What would be your financial plan? You may be left with a large inheritance. You may also have not been the main financial planner of the family. How would you go about accessing funds in a bank account or trust fund, for example? Without proper estate planning, which we’ll discuss later, you could be left in a financial situation that is tough to navigate.

Divorce can be a financially destabilizing event, often requiring the division of assets, legal fees, and more. When you factor in wealth, you must consider the complexities that come with dividing assets, such as real estate holdings, investment portfolios, and business interests. So, how can you best navigate this unexpected life event? For starters, a robust financial plan can be a major asset in helping smoothly navigate the significant life transition that comes with a divorce. It’s crucial to assess the impact of asset division on your long-term financial goals, including retirement planning and estate planning. Additionally, understanding the tax implications of asset transfers can help you strategize effectively to protect your wealth.

Disabilities caused by illness or injury could strike at any time. Financial planning for this unexpected life event can help those affected maintain the best possible standard of living, even in the event of lost income or wages. While you may have significant assets, ensuring that you have enough liquid funds to cover the immediate expenses of an unexpected life event is important to consider. When assessing your investment strategy, ensure a portion of your portfolio is easily accessible.

Did you know that 50% of all business transactions are involuntary? Disagreements between business partners can potentially threaten the business’s future, and therefore your personal financial goals as well. That’s why it’s important to have a detailed buy-sell agreement in place that outlines the terms under which a partner’s share of the business can be sold or transferred, preventing potential conflicts, ensuring business continuity, and protecting your legacy.

Economic downturns, natural disasters, and personal crises like job loss or major health issues can cause financial distress and unexpected cash flow needs. This can be mitigated by proactive measures that allow you to access capital when you need it most. So, let’s discuss ways that you can properly plan for unexpected life events.

When unexpected life events occur, a solid financial plan gives you more than just peace of mind. For many, it is the difference between having the right amount of money in place and not being able to properly pass wealth down to their families.

If you’re a business owner, ask yourself some of the following questions: Am I prepared to retire? Who will succeed me in leading the business? Do I need any support from my financial advisor? A comprehensive review of your business plan could be a great way to avoid any financial pitfalls caused by an unexpected life event such as death or disagreement.

On top of this, it is important to ensure you’re properly bankrolled for your retirement years. This will help you and your loved ones access money in the event of any unexpected life events which may occur in your later years.

Another great strategy for staying one step ahead of unexpected life events is estate planning. This is a crucial part of any long-term financial plan. It involves creating legal documents such as a will, trusts, and power of attorney, which provide clear instructions on how your estate’s assets are to be distributed.

Without an estate plan, your assets could be subject to lengthy probate processes, potentially causing financial strain and uncertainty for your loved ones. On top of this, you may be paying more in taxes on your estate than you could with the right plan. For example, passing down certain assets to loved ones before death could help you receive different tax breaks.

It is important to regularly review your estate plan with your BIP Personal Wealth Advisor to ensure it remains up-to-date at all times.

In some cases, insurance coverage can be the best way to deal with unexpected life events. Imagine a scenario such as a car accident or house fire. Without proper insurance coverage, the financial burden could be life-altering. Imagine if you and your family lost a vacation home to flooding, for example. Insurance could be the safety net that protects you and your family from significant financial loss due to unexpected expenses.

Consider life insurance in addition to traditional coverage such as home, auto, and health. If you’re the main earner of your family, life insurance can help keep your loved ones taken care of in the event of your unexpected passing or injury.

On top of the strategies listed above, planning for life’s unexpected events can be difficult alone. At BIP Wealth, our holistic and empathetic approach to financial planning ensures that every client’s financial needs are handled with personalized care. From inheritance management to estate organization to financial education, we help individuals, families, and businesses navigate the waters of unexpected expenses and life-changing events—whether you’ve recently lost a loved one, won the lottery, or sold a business. Through expert guidance and risk management, our team of experienced financial advisors will help keep your hard-earned assets protected under any circumstance. To learn more about our team or speak with an advisor, feel free to contact us at any time.

Unexpected life events include things such as injury, divorce, disagreement, and more. Financially, these events can be life-altering.

To best prepare for unexpected life events, it is important to have a financial plan in place ahead of time. This plan can include insurance coverage, income diversification, and estate planning to ensure you and your loved ones can access funds in times of need.

Those who assume unexpected life events will not occur to them tend to be the hardest hit. It is important to assume you will need financial support at certain times of your life, even if you never end up needing the help.

Examples of life-changing events include death, divorce, auto accidents, and plenty more. These events could bring financial and emotional stress.

This communication contains general investing information that is not suitable for everyone and is subject to change without notice. Past performance is no guarantee of future results and there is no guarantee that any views and opinions expressed will come to pass. The information contained herein should not be construed as personalized investment advice, tax advice, or financial planning advice, and should not be considered a solicitation to buy or sell any security. Investing in the stock market and the bond market involves gains and losses and may not be suitable for all investors. Indices are not available for direct investment.

ATLANTA — BIP Wealth is proud to announce the hiring of veteran Atlanta Estate Planning Attorney, Sarah Watchko to the role of Estate Planning Advisor. Over the past several years, BIP Wealth has collaborated with and referred clients to Sarah for Estate Planning creation and execution. Sarah will now lead the way in building out this important expertise in-house for BIP clients.

Sarah developed a passion during Law School for working with elderly clients and for clients who have a child with special needs. This was while she was working at the Elder Law Clinic at Wake Forest University in 2007. This led her to discover a career in estate planning, special needs planning, and elder law that could provide both intellectually demanding work and the opportunity to serve and improve the lives of others. Sarah finds immense joy in providing a high level of service, along with a calm and comforting demeanor to those navigating life’s challenges.

As a client of BIP, Sarah and her husband Jeff know firsthand the care BIP has for their clients but she never dreamed of joining the Team. “BIP’s CEO Bill Harris probably asked me about 15 – 20 times to consider joining the firm and I turned him down every time because I was happy in my previous role,” shared Sarah. “However, the more I learned about the role and what it could look like to build this for BIP’s clients from the ground up, it was clear this is an opportunity I couldn’t say no to.”

Sarah is particularly passionate about working with families navigating the complexities of special needs and hopes to elevate BIP as the go-to resource for those families in the Atlanta area. The greatest compliment she can receive is when a client shares, “You’ve taken the worry off my shoulders knowing the people I love most are protected.”

“We are honored that Sarah said yes to joining BIP and building out our Estate Planning Services! The care she provides clients aligns with our firm’s values perfectly,” shared Bill Harris, CFP®, Co-Founder & CEO of BIP Wealth. “I am excited for our future and all the ways this new internal capability will benefit the families at our firm in having peace of mind to be prepared for the future.”

An Atlanta native, Sarah lives in Roswell with her husband Jeff, son, daughter, and their loving mutt, Hank. She and her brother William attended Marist School in Atlanta. Both her brother and husband were collegiate athletes at Georgia Tech who went on to play professionally (the former football and the latter, baseball). Both families remain avid Georgia Tech fans. Sarah loves reading, spending time with friends and family, staying active, travel, and—in her rare free time—squeezing in a craft or baking project.