When most people hear “private credit,” their eyes glaze over somewhere between “senior secured” and “subordinated debt.” That’s understandable. The terminology sounds like it was designed to keep outsiders out. But the underlying concept is surprisingly intuitive once you see it laid out properly.

At its core, every private credit conversation comes down to one question: where does your money sit if something goes wrong?

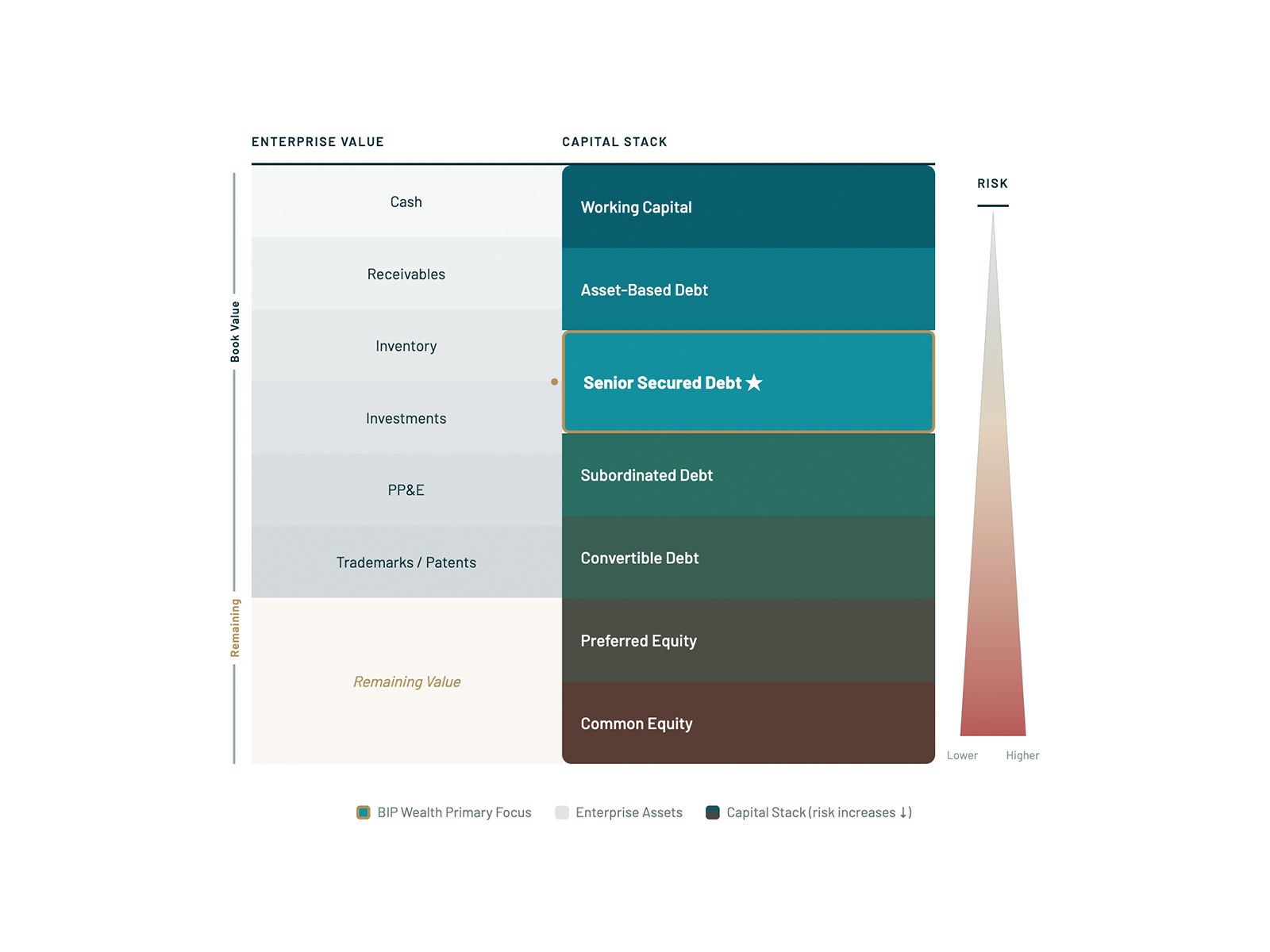

That’s what the capital stack tells you.

What Is the Capital Stack in Private Credit?

The capital stack is the hierarchy of claims on a company’s assets and cash flows. It determines who gets paid first, and who absorbs losses first, when a borrower runs into trouble.

Think of it as a line at the bank. The people at the front of the line, senior secured lenders, get paid first, no matter what. The people at the back of the line, common equity holders, only get paid if there’s anything left after everyone ahead of them has been made whole. The further back you stand, the more you might earn for your patience, but the greater the chance you walk away empty-handed.

The layers near the top of the capital stack, working capital and senior secured debt, get repaid before anyone else. They’re typically backed by tangible assets: cash, receivables, equipment, real property. The layers near the bottom, preferred and common equity, absorb losses first and get repaid last.

Every layer exists for a reason, and every layer earns a different return that reflects the level of risk the investor is accepting. The relationship between position and risk isn’t complicated, but it may be one of the most important concepts in private credit investing.

How Do the Layers of Private Credit Risk Compare?

The interactive graphic below maps out the full capital stack alongside a company’s enterprise value: the assets that back these obligations. Take a moment to hover over each layer to see what it means and how it relates to risk and return.

Here’s a quick summary of each layer, from lowest risk to highest:

- Working Capital sits at the very top. These are short-term obligations that fund day-to-day operations like payroll, supplies, routine expenses. They’re repaid first and carry the lowest risk.

- Asset-Based Lending involves loans secured by specific collateral like equipment, receivables, or inventory. If the borrower can’t pay, the lender has a direct claim on those assets.

- Senior Secured Debt is backed by collateral and holds priority over all other long-term creditors. In a liquidation scenario, senior secured lenders are first in line to recover their capital from the company’s assets. This is where BIP Wealth concentrates its private credit strategies.

- Subordinated Debt gets repaid only after senior lenders have been made whole. The higher yield on subordinated debt compensates investors for accepting that lower priority position.

- Convertible Debt is a hybrid instrument that starts as a loan but includes the option to convert into equity under certain conditions. It offers some downside protection with participation in the company’s upside.

- Preferred Equity represents ownership with priority over common shareholders for dividends and distributions. It carries more risk than any form of debt but offers more predictable income than common equity.

- Common Equity is last in line for everything—distributions, liquidation proceeds, everything. Common shareholders bear the greatest risk but also have the greatest potential for return if the company performs well.

Why Does Senior Secured Direct Lending Attract So Much Attention?

Headlines tend to focus on the extremes. Equity investors making a fortune or losing everything generates clicks. But the most interesting part of the capital stack for many investors is the middle, specifically, senior secured direct lending.

Here’s why. Senior secured loans sit high enough in the stack that the borrower’s tangible assets serve as a meaningful safety net. If a company can’t make its payments, senior secured lenders have priority claim on those assets ahead of subordinated lenders, ahead of equity holders, ahead of everyone except the most short-term obligations at the very top.

At the same time, these loans may offer yields that meaningfully exceed what most traditional fixed income instruments have historically provided. That combination, repayment priority plus competitive income potential is what has drawn significant institutional capital to this space.

The tradeoff? Liquidity. Unlike a publicly traded stock you can sell on an exchange in seconds, private credit investments are typically held in evergreen fund structures with specific redemption windows and potential limitations on withdrawals. That reduced liquidity is actually part of the design which may help prevent the kind of forced selling that can destabilize public market strategies during periods of stress. However, investors should understand that their ability to access capital may be limited during certain periods.

How Does Knowing the Capital Stack Help You Evaluate Private Credit?

This is the part where the capital stack visual becomes genuinely useful as an educational tool. When someone says they “invest in private credit,” that phrase alone doesn’t tell you much. A subordinated debt fund and a senior secured direct lending fund are both technically private credit, but they occupy very different positions in the repayment line.

Subordinated debt may earn a higher coupon because the investor is accepting more risk—they’re further back in line if the borrower encounters difficulties. Convertible debt adds another dimension: it starts as a loan but can transform into ownership under certain conditions. Mezzanine financing sits in between, bridging the gap between debt and equity with characteristics of both.

Each of these strategies has a place in portfolio construction. But knowing which layer you’re investing in and understanding why it may pay what it pays can be the difference between a thoughtful allocation and a decision based on a label.

How Does BIP Wealth Approach Private Credit?

BIP Wealth’s private credit strategies concentrate on diversified, senior secured, direct lending backed by private equity sponsors. In practical terms, that means lending to established, middle-market companies where a large investment firm has performed due diligence, negotiated protective covenants, and has its own capital at stake alongside investors.

The objective isn’t to chase the highest available yield on the capital stack. It’s to target the layer where the historical risk-adjusted characteristics have been favorable, and where the structural protections provide a foundation for confidence across varying economic environments.

BIP Wealth complements this core approach with exposure to asset-based lending and, selectively, other strategies when they align with a client’s overall financial plan and risk tolerance.

The goal is never to maximize a single variable. It’s to construct a portfolio designed to seek consistent, reliable income without taking on more risk than the investor’s situation warrants.

Private credit strategies involve risks including the potential loss of principal, limited liquidity, and sensitivity to interest rate changes. Past performance of any strategy is not indicative of future results.

The Bottom Line

The capital stack isn’t just an academic framework, it may be the single most important factor in understanding what you actually own when you invest in private credit. Before evaluating any fund, any headline, or any investment opportunity, start with one question: where in the line am I standing?

If you understand that, everything else falls into place.

If you’d like to learn more about how private credit may fit within your overall portfolio, reach out to us to connect with a BIP Personal Wealth advisor.

This post is provided for informational purposes only and should not be construed as investment advice or a recommendation to buy or sell any securities. Ideas and opinions expressed represent the views of BIP Wealth and are subject to change without notice. Private credit investments involve risks, including the potential loss of principal. Privately traded offerings may only be available to investors who meet certain qualification statuses. There can be no assurance that actual outcomes will match any expected returns. Past performance is not a guarantee of future results. All investing involves risk, including the possible loss of principal. BIP Wealth is a registered investment advisor. Registration with the SEC does not imply a certain level of skill or training.