Welcome to our 2026 Annual Market Report with Eric Cramer, CFP®, CFA®, BIP Wealth’s Chief Investment Officer. For this year’s presentation, Eric starts with an honest scorecard of how BIP’s 2025 investment themes played out, recaps what happened in markets around the globe, and makes the case for why the economic landscape is shifting in ways that matter for your portfolio.

In case you missed the live presentation, we’ve summarized Eric’s main talking points below. You can also watch the recording of the presentation below.

Grading Our 2025 Investment Themes

Eric opened by going back to the four key investment themes BIP Wealth identified for 2025 and gave an honest accounting of how each played out.

Theme 1: Brace for a Tech/Crypto Crash

Eric acknowledged this one made BIP Wealth CEO Bill Harris a little bit nervous when he used the word crash—but Eric’s reasoning was sound. A lot of tech and crypto exposure was leveraged, and as we saw during the housing crisis, leverage in any direction can be a real problem.

By the end of Q1, it looked like Eric was going to be right—and he admitted he honestly was not excited about that. Tech stocks got hit hard in the first quarter. Tesla fell 35.83%. NVIDIA fell 19.29%. But then something remarkable happened: markets turned the corner and several of those same stocks came roaring back. Alphabet, for example, went from down 18% in Q1 to up more than 65% for the full year. Berkshire Hathaway flipped the other direction, shining in Q1 when tech was falling, then giving some of that back over the remaining three quarters.

The ultimate verdict? “We kinda got close to a crash,” Eric said, “but crash is probably too strong a word.” It was a significant downturn followed by a remarkable recovery.

Source: Source: Morningstar, Worldperatio.com, PE Data as of 12/31/2024, Returns Data as of 3/31/2025, 12/31/2025

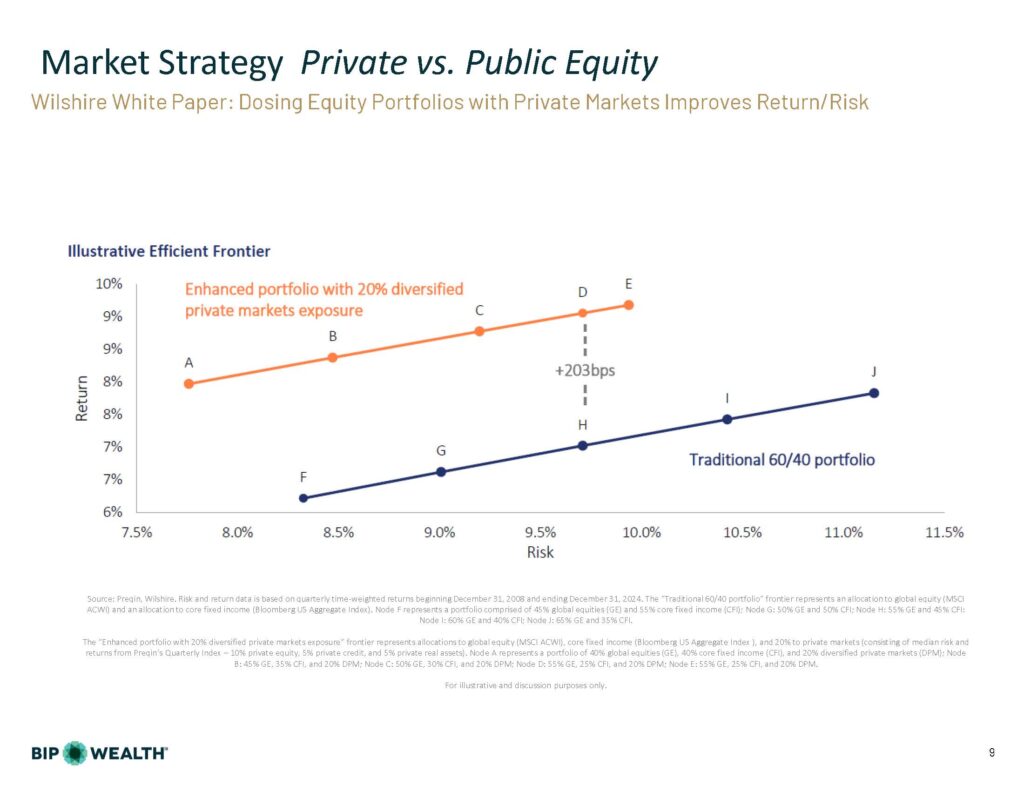

Theme 2: It’s Time to Diversify

The public stock market’s top 10 stocks represented about a third of the entire market’s value at the start of 2025—and even a little more by the end. While most investment managers typically think of diversification in terms of the public markets, Eric made the case for private markets as the most meaningful diversification tool available.

On the private equity side, Eric shared compelling data: over longer periods, private equity has delivered returns roughly four percent higher per year than public equity. And crucially, the two asset classes don’t move in lockstep—which means holding both yields lowers volatility than holding either one alone, as the markets are not directly correlated.

He also highlighted a significant change in how investors can access private markets. The traditional model—committing to a fund, experiencing years of capital calls, then waiting another decade for your money back—is giving way to a new breed of vehicles called Evergreen Funds, including BDCs and interval funds. These allow you to put money in when you want and request liquidity in advance of when you need it. Eric called this a game changer for us and for you and noted that the newest versions have little to no paperwork.

Source: Source: Preqin, Wilshire. Risk and return data is based on quarterly time-weighted returns beginning December 31, 2008 and ending December 31, 2024. The “Traditional 60/40 portfolio” frontier represents an allocation to global equity (MSCI ACWI) and an allocation to core fixed income (Bloomberg US Aggregate Index). Node F represents a portfolio comprised of 45% global equities (GE) and 55% core fixed income (CFI); Node G: 50% GE and 50% CFI; Node H: 55% GE and 45% CFI: Node I: 60% GE and 40% CFI; Node J: 65% GE and 35% CFI.

The “Enhanced portfolio with 20% diversified private markets exposure” frontier represents allocations to global equity (MSCI ACWI), core fixed income (Bloomberg US Aggregate Index ), and 20% to private markets (consisting of median risk and returns from Preqin’s Quarterly Index – 10% private equity, 5% private credit, and 5% private real assets). Node A represents a portfolio of 40% global equities (GE), 40% core fixed income (CFI), and 20% diversified private markets (DPM); Node B: 45% GE, 35% CFI, and 20% DPM; Node C: 50% GE, 30% CFI, and 20% DPM; Node D: 55% GE, 25% CFI, and 20% DPM; Node E: 55% GE, 25% CFI, and 20% DPM. For illustrative and discussion purposes only.

Theme 3: Financial Planning is Critical

Eric noted he was pleased to see that many BIP Wealth clients got their financial plans updated in 2025. This remains a core part of the BIP approach: there are often risks that can be identified and mitigated with the right plan in place. No further commentary needed — just a strong endorsement to keep your plan current.

Theme 4: Safer Assets Can Be Productive

The era of earning inflation-beating returns on the safest possible assets has narrowed significantly. Short-term treasuries are currently yielding around 3.6%, and Eric doesn’t expect the Federal Reserve to lower rates for much of, or possibly all of 2026. They held at the last meeting, and the futures market puts any cut likely at mid-year at the earliest. He noted there’s even a scenario where rates could move higher.

For clients in high tax brackets holding treasuries in taxable accounts, the margin over inflation has become thin. That’s led BIP to look more closely at municipal bond strategies, which Eric described as increasingly attractive. Because so many states have balanced budget requirements, he went as far as suggesting that munis may be the new treasuries in terms of safety.

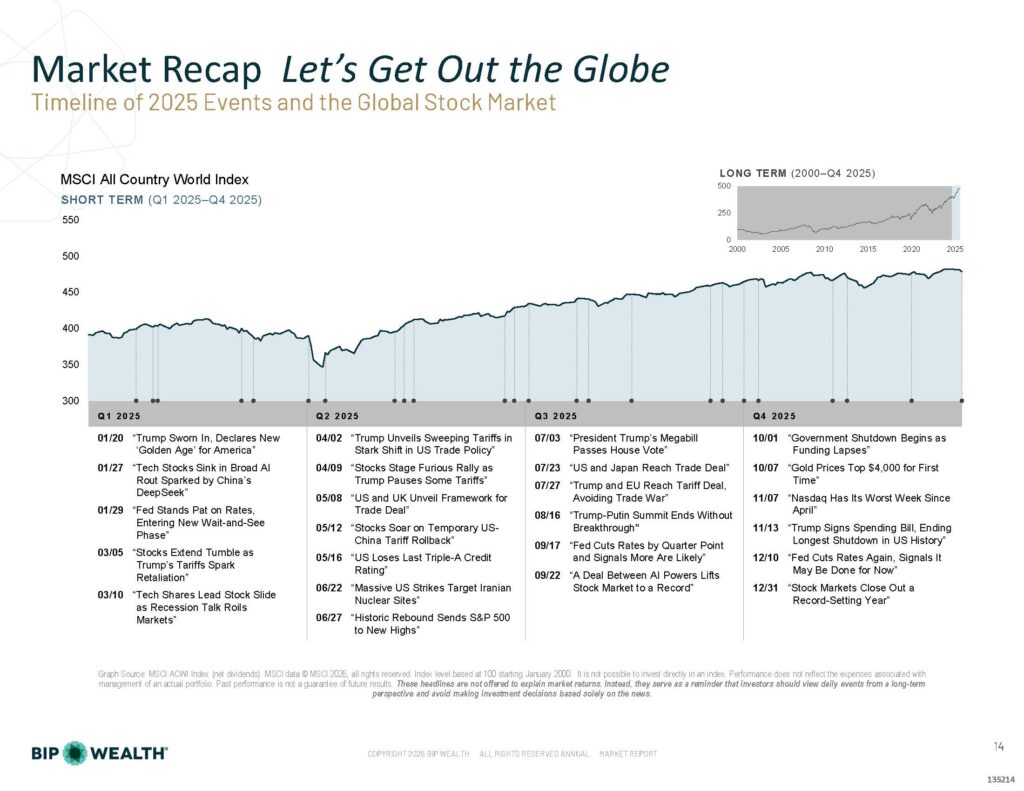

The Market Recap: Let’s Get Out the Globe

The Year That Felt Like Surgery Without Anesthesia

Someone told Eric that 2025 felt “a bit like surgery without anesthesia.” The year was packed with headlines: tariff announcements, geopolitical moves, government shutdowns, market swings. But if you missed the news and just looked at the value of your investment accounts, you might have blinked and missed the fact that there was even a downturn. Markets dipped on tariff news early in the year and came right back. This is the third consecutive year of a strong global stock market, and Eric noted that for many clients, their own balance sheets are about as big as they’ve ever been.

Source: Graph Source: MSCI ACWI Index (net dividends). MSCI data © MSCI 2026, all rights reserved. Index level based at 100 starting January 2000. It is not possible to invest directly in an index. Performance does not reflect the expenses associated with management of an actual portfolio. Past performance is not a guarantee of future results. These headlines are not offered to explain market returns. Instead, they serve as a reminder that investors should view daily events from a long-term perspective and avoid making investment decisions based solely on the news.

The Best Returns Were Outside the U.S.

Even though the U.S. stock market had a terrific year—returning 17.15%—the best returns in 2025 came from outside the country. International developed market stocks returned 31.85% for the year. Emerging market stocks returned 33.57%, nearly double what the U.S. produced.

A big part of the story is the weakening U.S. dollar. When the dollar weakens, foreign currencies strengthen. And when you invest in overseas equity markets, you’re really investing in both a foreign stock market and a foreign currency. When both go up together, you get the compounded effect of those two phenomena. That’s how you get these impressive international numbers.

It’s worth noting, however, that a weaker dollar cuts both ways. It can help U.S. manufacturers whose goods become cheaper overseas, but it makes imported goods more expensive for the rest of us. More dollars to buy the same goods: that’s the definition of inflation.

The Market Outlook: Revaluing Debt and Currencies

Eric warned this section would feel a little bit like an econ class, but the material is important, and he walked through it in a way that’s worth unpacking.

Japan and the Carry Trade: A Crisis in the Making?

One of the more fascinating and underappreciated dynamics affecting global markets right now is what’s happening in Japan. For decades, Japan had ultra-low or even negative interest rates. Home safes became popular in Japan because at least your money didn’t shrink sitting in a safe. But in a negative rate environment, sophisticated financial players could borrow in Japanese yen for next to nothing, invest in U.S. Treasuries at 4%, and pocket a comfortable margin. This was the Japanese carry trade, and it reached into the trillions of dollars across decades.

That trade has more or less evaporated. Japan’s interest rates have skyrocketed, borrowing costs are far higher, and the margin that made the trade profitable is gone. This is a real problem and it’s one reason why the U.S. could see pressure to intervene in currency markets, which would further weaken an already weakened dollar.

Consumer Confidence: A Tale of Two Americas

The consumer confidence data tells a nuanced story. The “present situation” index is holding up better than the “expectations” index—both trending downward, but the present looks better than the future. Eric noted he often encounters this disconnect in conversations with clients: “I’ll ask them how they’re doing, and they may talk about pessimism about the economy. But when we get down to how they’re doing personally, they’re often doing great.”

Part of what explains that gap is who drives consumer spending. The top 20% of earners are responsible for about half of all consumer spending in the U.S.

Here’s a concept worth sitting with: Eric learned in business school that the stock market reflects the state of the economy. But he thinks that may have flipped. Today, if the stock market is doing well and your balance sheet is at record highs, you feel good about spending—and the economy follows. The tail is wagging the dog.

For those in the top tier of earners and asset holders, this dynamic is likely to persist. If there’s a problem with interest rates and the Fed has to come to the rescue printing money, if you’ve got an investment portfolio, you’re probably going to be fine.

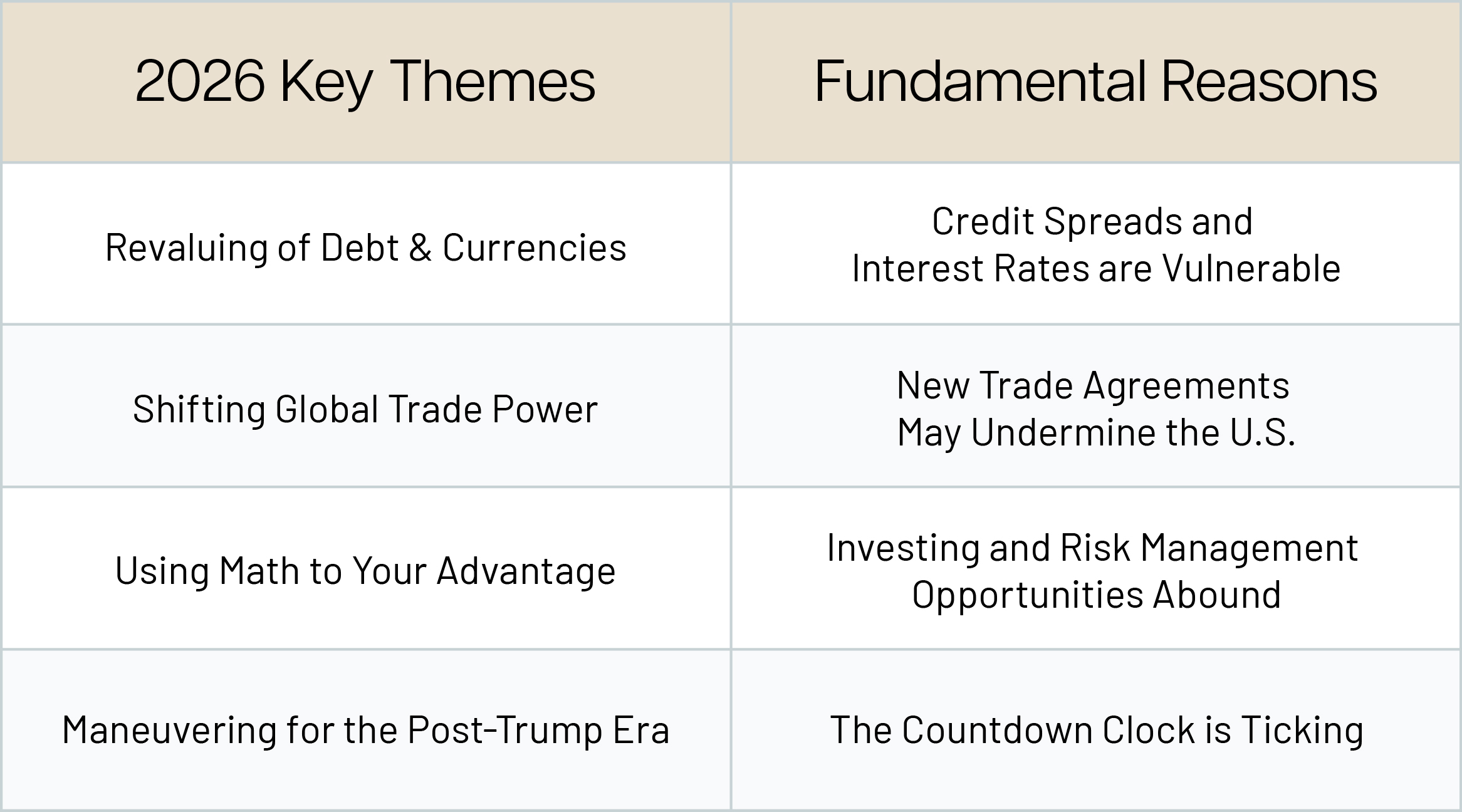

Our 2026 Key Investment Themes

Looking ahead, BIP Wealth has identified four themes that will shape our investment approach this year:

- Revaluing of Debt & Currencies: Credit spreads and interest rates are vulnerable.

- Shifting Global Trade Power: New trade agreements are being written around the globe that may increasingly leave out the United States. This has real implications for the dollar’s global dominance, and it’s something Eric intends to watch closely and update clients on throughout the year.

- Using Math to Your Advantage: Throughout 2026, BIP will share specific “nuggets of math” that could improve your return, lower your risk, or improve your overall financial situation.

- Maneuvering for the Post-Trump Era: The countdown clock is already ticking, and both political parties are maneuvering now. The 2026 midterm elections are going to be a very big deal, with potentially significant effects on tax rates, monetary policy, and fiscal policy.

Final Thoughts from Eric Cramer, CFP®, CFA®

Eric closed with a broader perspective on the moment we’re in. The world is changing fast—AI, global trade, geopolitics—and that’s changing the landscape for investing in ways that require expertise and attention to evidence rather than headlines.

America is divided, economically as much as politically. The bottom half of Americans don’t own a share of stock. The top earners hold most of the assets and drive most of the spending. For BIP Wealth clients, that divide is actually somewhat protective, but it also creates instability that we need to plan around.

“BIP Wealth is dedicated to using the best evidence available to help you meet your financial goals in a future that doesn’t look like the past,” Eric said. “This is when expertise and insight matter most.”

Don’t be surprised if your Personal Wealth Advisor brings new ideas to your next conversation. BIP Wealth is actively building and deploying new tools to help clients navigate everything this year may bring. If you’d like to speak with an advisor about your portfolio or learn more about how our 2026 themes might affect your financial plan, we’d love to hear from you.

This communication contains general investing information that is not suitable for everyone and is subject to change without notice. Past performance is no guarantee of future results and there is no guarantee that any views and opinions expressed will come to pass. The information contained herein should not be construed as personalized investment advice, tax advice, or financial planning advice, and should not be considered a solicitation to buy or sell any security. Investing in the stock market and the bond market involves gains and losses and may not be suitable for all investors. Indices are not available for direct investment. Certain private market investments are subject to qualification thresholds and are subject to significant risks, including liquidity risk.